What Happens When You Spend Money and How to Save Smartly?

Frequently asked question is what is when you spend or use money? Financial well-being is mostly dependent on the management of money. There is a huge difference in spending or using money. Using money is to maximize the value and satisfaction usually only on the necessities. While spending money means buying decisions are overwhelmed by emotions on luxury items. However, the act of spending sometimes seems like an emotional trip. Understanding what happens when you spend money will help you make better decisions and reach your financial objectives, from the excitement of purchasing something new to the realization that you might have spent too much. This post will go over the psychological and pragmatic sides of spending, discuss typical spending traps, and offer doable advice to enable wise savings.

Introduction

Whether you’re grocery shopping, paying bills, or treating yourself to a new device, spending or using money is a regular activity. Spending is really the act of trading money for experiences, goods, or services. Although life is inevitable, your spending behavior will significantly affect your long-term objectives and financial stability.

Good financial management is about making sure you have the means to save for the future, invest in possibilities, and manage crises, not only about covering needs. Overspending can ruin your financial situation and reduce your income for needs, including house purchases, retirement savings, or emergency fund building. Unchecked spending could also cause debt, worry, and a cycle of financial insecurity.

The good news is that knowledge of the mechanics of expenditure helps one create better habits and make wise decisions. First, let’s look at the psychology of financial decisions.

The Psychology of Spending Money

Your brain does an amazing procedure when you spend money. Spending releases dopamine, the “feel-good” hormone, which can set off instantaneous satisfaction. This is why dining at a luxury restaurant or purchasing a new pair of shoes could make the occasion so fulfilling. But this fleeting pleasure often fades, resulting in a phenomenon known as the “hedonic treadmill,” in which one seeks out fresh purchases to keep that pleasure.

Emotional Triggers and Spending

Emotions rather than needs motivate you to spend money. People buy to rejoice, relax, or fight boredom as well as to handle stress. To feel successful, someone can indulge in a lavish vacation following a demanding year at work or purchase an expensive device. If not well-considered, these expenditures might tax you financially even if they could provide some momentary comfort.

Marketing and Sales Tactics

Retailers and advertisers are experts in changing spending decisions which makes you to spend money. Strategic store layouts, “buy one, get one free,” and even limited-time specials are meant to inspire you to spend more. Ever noticed how bread and milk are kept towards the rear of stores by supermarkets? This guarantees that on your way, you pass by enticing munchies and other non-essentials.

Preventing unneeded expenditure depends on an awareness of these psychological and marketing impacts. Understanding the causes of your spending patterns will help you to control your financial situation.

Common Traps When Spending Money

Common traps can even be found among those who are most economical which makes you to spend money. Let’s look at some of the most common mistakes and how one could prevent them.

- Impulse Buying

Unplanned purchases—often driven by emotions or appealing displays—are known as impulse buying makes you to spend money. For example, adding things to your cart during a flash sale could seem safe, but those little, unexpected charges can mount up. Slick deals’ research revealed that Americans spend more than $5,400 a year on impulse purchases, therefore highlighting the financial influence of this behavior.

- Emotional Spending

Purchasing items to help you deal with emotions such as stress, grief, or even happiness amounts to emotional spending leads you to spend money. For instance, someone might explain an expensive dinner they treat themselves to following a demanding day as a reward. While occasional treats are okay, regular emotional spending can cause financial difficulty and guilt.

- Lack of Budgeting

It’s easy to overlook your spending without a budget which leads you to spend money unnecessarily. You might unintentionally overspend on non-essentials while ignoring savings or critical debt. For instance, regular dining out without understanding the expenses relative to home cooking can lead to a notable financial difference.

- Falling for “Deals” That Aren’t Deals

To generate steadfastness, retailers sometimes employ strategies, including bogus discounts so consumer can spent money without thinking twice. For instance, marking up an item’s price before offering a “50% off” sale makes the discount seem more appealing, even if the final price isn’t a true bargain. Knowing these techniques helps you avoid pointless purchases.

How to Avoid Overspending

Although it can feel like a difficult habit to break, We can avoid overspending with the correct techniques and wise decision-making of your money. These are some possible suggestions to cut pointless expenses and maximize savings.

- Create and Stick to a Budget

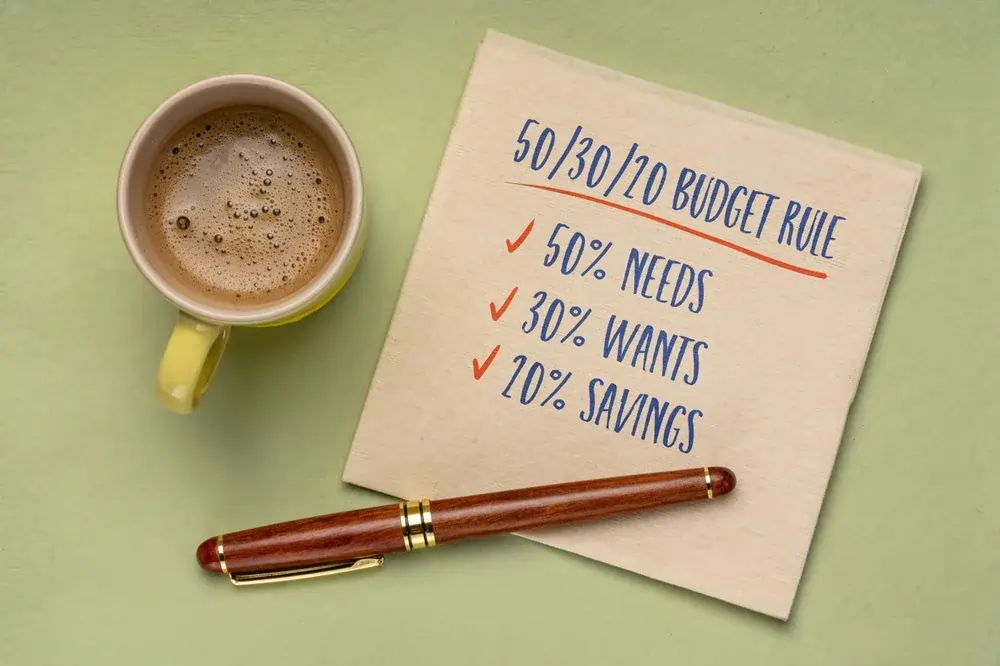

The basis to avoid over spending is a well-considered budget. Start by noting your fixed expenses—rent, utilities, debt—as well as your income. Set aside some for savings, then split the remaining amount for optional use. The 50/30/20 Rule (50% needs, 30% wants, 20% savings), among other tools, helps to streamline this procedure.

Mint, YNAB (You Need A Budget), and Pocket Guard are among the budgeting apps that let you monitor your spending in real-time and make sure you stay under your means.

- Use Financial Tools

To avoid over spending financial tools and expense monitors give a thorough understanding of where your money is going and not to over spend. They classify your spending, thereby enabling you to find places for cutbacks. Some programs also keep you responsible by sending alarms as your spending limit approaches.

- Practice the 24-Hour Rule

The 24-hour Rule is one good way to limit impulse shopping. Wait 24 hours before committing if you are inclined to buy. This cooling-off period lets you assess if the purchase is really required or only a passing need. This rule help in cause of not to over spend.

- Avoid Temptation

Cut temptations by unsubscribing from advertising emails, avoiding perusing shopping websites without a stated goal, and avoiding malls or stores when you’re feeling emotional. Establishing limits will enable you to fight the seduction of pointless consumption. By avoiding temptation you will understand the theory of not to over spent.

- Plan Purchases in Advance

Especially for large-ticket items, organizing your purchases guarantees you are making wise choices. If you are beginning a collection, for example, study costs, create a budget, and give quality top priority above volume. This method guarantees your happiness with your decisions and helps you avoid overspending.

Smart Saving Strategies

Although avoiding overpaying is absolutely vital, as vital is understanding how to save wisely. Saving is about giving your financial goals a top priority and choosing deliberately; it does not imply sacrificing yourself. Here are some clever tips not to over spend.

- Automate Your Savings

Every payday, arrange automated transfers to a savings account. This guarantees your regular savings free from Temptation to spend the money elsewhere. Many banks provide instruments to automatically save money, therefore streamlining the procedure and allows not to do over spending.

- Build an Emergency Fund

Covering unanticipated costs such as medical bills or car repairs, an emergency fund serves as a financial safety net. Save three to six months’ worth of living expenditures in a separate, easily accessible account. This cushion keeps you from depending on loans or credit cards in a crisis.

- Take Advantage of Discounts and Rewards

Smart saving is not about never spending. Search for strategies to maximize value with cashback offers, loyalty programs, and discounts. For routine purchases, for example, utilizing a credit card with cashback incentives can help you save money while still meeting your demands. Its called smart management without over spending.

- Set Clear Financial Goals

If you have a clear objective in mind, saving is simpler. Whether your objective is to buy a house, travel, or retire early, it will keep you driven. Divide your goal into manageable chunks and monitor your development often.

- Learn to Differentiate Wants from Needs

Smart saving is mostly dependent on an awareness of the differences between requirements and wants. Ask yourself before you buy whether it’s a need or a luxury. This habit helps you cut unneeded spending and rank important bills.

Specific Tips for Starting a Collection without Overspending

Whether your collection consists of coins, artwork, books, or unique objects, beginning a trip is fascinating. But if you don’t have a good plan, this pastime may soon get costly. Mindful planning is the secret to loving your collection without over spending on collection. These thorough guides on beginning a collection without going over budget follow below.

- Research and Set a Clear Budget

Research is crucial even before starting any collection to prevent overspending. Learn about trends, rarity, and availability; also, know the market value of the objects you are considering. For instance, if you are gathering antique comic books, study condition grading and how it influences price.

After your investigation, create a well-defined budget. Choose how much you are ready to commit to your collection every month or every three months. Apart from preventing overspending, a budget enables you to give excellent items top priority over impulse purchases. For example, you can decide to save for one outstanding piece instead of multiple average objects.

- Start Small and Focus on Quality over Quantity

When beginning a collection by keeping in mind not to over spend much, it’s easy to buy a lot of things fast, but this usually results in clutter and regret. Start with just a few well-chosen objects. If you are beginning a coin collection, for instance, concentrate on gathering coins from a given era or region instead of trying to gather everything at once.

More than anything, quality counts. Often, both personally and financially, a well-curated collection of high-quality objects has greater value than a sizable collection of poor-quality objects. Spend some time locating objects that really speak to you and fit inside your means.

- Avoid “Fear of Missing Out” on Deals

Starting a collection often involves a frequent mistake known as fear of missing out (FOMO) which is not a good way to prevent unnecessary spending. Rare finds, limited-time discounts, or intense bidding can force you to spend more than you intended. Not every offer, meanwhile, is as fantastic as it sounds. Ask yourself, before you buy:

- is this item absolutely vital for my collection?

- Could I find it somewhere else for less?

- Does purchasing this fall within my means?

Learning self-discipline and patience will help you stay from overspending from FOMO. Remember, the search is part of the fun of collecting, so avoid rushing the process.

Do You Need a Certain Amount of Money to Save?

One of the most frequent asked question regarding saving is that do you need a certain amount of money to save? Actually, saving is more about disciplined behaviors than about the money you make. Anyone, regardless of their income, can develop a saving habit in the following way.

- Saving on a Low Income

One can save even with a small salary by choosing deliberately which is the proof of you don’t need a certain amount of money to save. Start by noting little areas you might cut back on. Making coffee at home instead of buying it every day, for instance, can save hundreds of dollars a year.

Take this instance: Maria makes 2,500 bucks a month. She pays her utilities, rent, and other bills and then saves $100 a month. Maria saves $1,200 throughout the year, proving that regularity counts more than daily savings.

- The Concept of “Paying Yourself First”

“Pay yourself first” involves approaching savings as a non-negotiable outlay, much like utilities or rent. This concept does not require a certain amount of money to implement. Before you spend anything else, set aside a part of your salary for savings. Direct deposit of this method into a savings account guarantees consistency and eliminates the need to overlook saving.

If you choose to set aside 10% of your income, for instance, and make $3,000 a month, you will save $300 before considering any spending. This strategy puts your financial situation first and, over time, helps you create riches.

Practical Saving Techniques

Important question is how do you save? Effective saving need not be difficult. Following a few sensible strategies will help you create a financial safety net and yet enjoy life. These ideas will help you get going:

- Automate Your Savings

One of the simplest strategies to get the answer of how to spend is automation. Many banks have automated transfer capabilities wherein some of your payback goes into a savings account. Automating saves forces you to give savings top priority without thinking about it.

If you get $1,000 biweekly, for instance, arranging an automated transfer of $50 each pay will easily save $1,300 a year.

- Reduce Unnecessary Expenses

Reducing non-essential spending helps you to realise how to save. Start by looking at your spending patterns and noting where you may cut expenses. Typical examples include cancelling inactive subscriptions.

- Cooking at home rather than dining out.

- Choosing generic names above name brands.

Little adjustments like cutting entertainment costs by $50 a month can pile up over time to be really large.

- Follow the 50/30/20 Rule

A basic budgeting tool, the 50/30/20 Rule distributes your money as follows:

- 50% for needs, including groceries, utilities, and rent.

- 30% for Wants: Not necessarily yet fun hobbies like dining out.

- Twenty per cent for savings—building an emergency fund, making investments, or debt pay-off.

Following this guideline helps you to reconcile living for the present with future preparation. For instance, if your monthly salary is $4,000, you would set aside $800 for savings, $1,200 for wants, and $2,000 for needs.

Bad Ways to Prevent Unnecessary Spending

Although budgeting is important, some techniques might backfire and are not a good way to prevent un necessary over spending. These are some things not to do while seeking to cut unneeded expenses:

- Cutting Out All Pleasures Entirely

While cutting all discretionary spending seems like a quick fix, it usually causes irritation and binge-buying and not a good way to prevent unnecessary over spending. For example, after a month of deprivation, you may find yourself splurging on a pricey restaurant dinner if you quit dining out totally.

One better strategy is to set aside sporadic treatment money. Savouring little pleasures—such as a movie night or a monthly coffee trip—keeps you inspired to follow your general savings goal.

- Ignoring Realistic Goals for Budgeting

Unrealistic budgets is not a good way to prevent over spending. For instance, you would either overspend or feel demoralized if you set aside just $50 for groceries in a month, but your real spending is more like $200. Rather, establish your budget in reasonable numbers that reflect your way of living and provide space for changes.

Conclusion

Control of your expenditure and saving behavior does not call for extreme actions or a high income. Whether you are beginning a savings account or a collection, the secret is to approach your money with discipline and awareness.

Essentially:

- Start Your Collection Sensibly: Research, create a budget, give quality top priority, and stay away from FOMO.

- Saving is for everybody: Establish disciplined behaviors, including initially paying yourself and automating savings.

- Apply pragmatic approaches: Use systems like the 50/30/20 Rule to eliminate unneeded spending without compromising fun.

- Steer clear of destructive approaches: To avoid burnout, balance saving with consumption.

Little, consistent actions today can result in major financial stability going forward. Recall that it’s more about how purposefully you utilize your income than about how much you make.

If these ideas were useful, forward this post to friends or leave a note below on how you handle saving and expenditure.